JOHANNESBURG (miningweekly.com) – The acquisition of the Moab Khotsong gold mine represents a significant list of advantages for Harmony Gold, the company outlined in an investor brief on Wednesday.

The Johannesburg Stock Exchange-listed gold mining company calculates that inclusion of the Moab Khotsong operations the company acquired from AngloGold Ashanti in October, for $300-million, provides major earnings, cash flow, grade and cost fillip.

Harmony, headed by CEO Peter Steenkamp, describes Moab Khotsong as a safe, profitable producer with strong margins that will help the company on the road to its aspiration of becoming a producer of 1.5-million ounces of gold a year.

The inclusion of Moab Khotsong immediately gives Harmony a 20% lower all-in-sustaining cost profile in South Africa.

Inclusion in Harmony’s 2017 financial results would have given earnings before interest, taxes, depreciation and amortisation a 42% surge, 62% more free cash and 25% more South African production.

It gives the company’s underground recovered grade a 65% better position and makes Harmony a top three free cash generator.

Harmony’s proven record in mining high-grade pillar mining positions the company well at both Moab Khotsong and its associated Great Noligwa gold mine, located on the Far West Rand, south-west of Johannesburg.

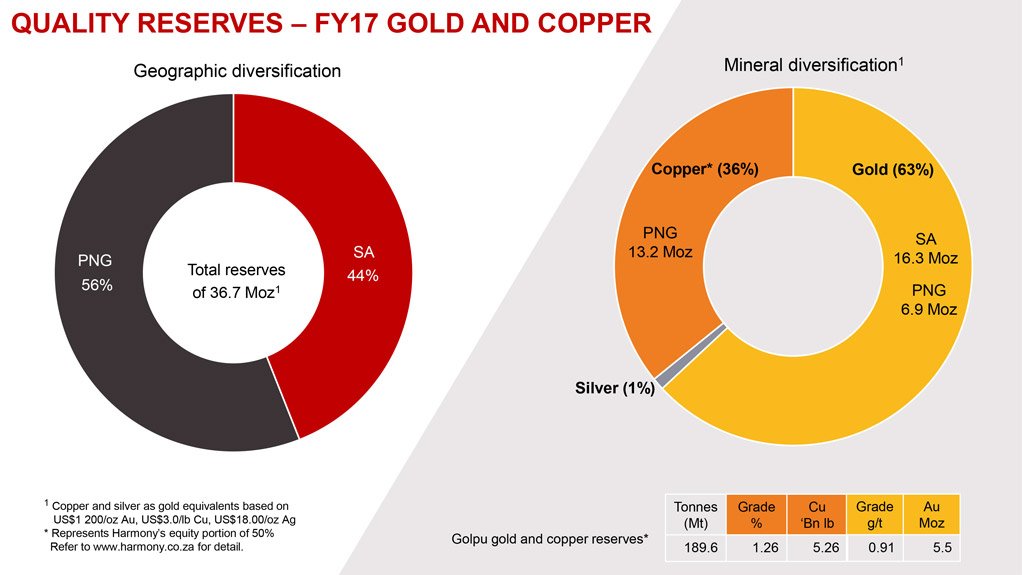

The life-of-mine grade forecast for Moab Khotsong is 8.2 g/t, taking average Harmony grade across its nine underground and one opencast mine to 5.7 g/t.

More immediate growth is also provided by large low-risk, low-cost tailings retreatment being part of the Moab Khotsong acquisition, as well as the Zaaiplaats project.

Moab Khotsong, one of the newest of South African deep-level mines, has three vertical shafts with the orebody divided through major faulting into three distinguishable blocks referred to as the top mine of Great Noligwa, the middle mine and Zaaiplaats.

The Great Noligwa mine was merged with Moab Khotsong in 2014, following which operations were collectively referred to as Moab Khotsong. Great Noligwa started production in 1968 and Moab Khotsong started producing in 2003.

The geology at Moab Khotsong is structurally complex, with large fault-loss areas between the three main mining sites.

The $300-million purchase price was funded by $100-million from existing bank facilities and $200-million in committed bridging finance. Intended now is to cover that by way of $100-million from internal cash resources and another $100-million in equity capital from a likely private share placement or alternatively a rights issue.

Harmony, which is fully black empowered and committed to advancing transformation, will empower the Moab Khotsong transaction with an employee share ownership plan, community trust and a black industrialist supplier base.

Harmony sees its investment cases increasing its potential for a re-rating, given its delivery at Hidden Valley and value realisation at Golpu, both in Papua New Guinea.

The company’s favourable gearing to the rand gold price and negligible debt position compared with its major peers also offer potential share price uplift.

It expects Hidden Valley to be producing at a rate of 180 000 oz/y in its 2019 financial year at an all-in sustaining cost (AISC) over the six year life-of-mine of $850/oz.

The 35-year Wafi-Golpu also provides access to 8.6-million tonnes of copper and mining from low-cost block-caving.

Harmony is guiding a production of 1.1-million ounces of gold in its 2018 financial year at an average grade of 5.18 g/t and an AISC of $1 180/oz.

Edited by: Creamer Media Reporter

EMAIL THIS ARTICLE SAVE THIS ARTICLE

ARTICLE ENQUIRY

To subscribe email subscriptions@creamermedia.co.za or click here

To advertise email advertising@creamermedia.co.za or click here